%20(16).svg)

.png)

.svg)

.svg)

The $300 billion stablecoin market has proven one thing conclusively: when you build financial infrastructure that works, people use it. Over 50 million users now hold or transact with stablecoins, generating more than $27 trillion in annual transaction volume across chains.

https://x.com/cointelegraph/status/1974059621460353444?s=46

Stablecoins broke out of the “trading collateral” status

2025 was about “normalizing” stablecoins. The total market capitalization hit $300 billion - a threshold that suddenly put stablecoins in the same conversation as systemically essential financial infrastructure. Transaction volumes reached what you'd legitimately call "payment network" scale. McKinsey cited $27 trillion in annual transaction volume. Sure, in the grand scheme of global finance, that's still a fraction, less than 1% of daily transfers worldwide. Despite that, stablecoin supply doubled in the past 18 months and we finally saw digital assets escape their crypto-native bubble into real-world applications.

For years, stablecoins were hoarded as trading collateral or portfolio hedges. In 2025, they increasingly moved. That evolution from “store of value” to actual payment rails is what transformed stablecoins to genuine economic infrastructure. This growth wasn't accidental; it was accelerated by regulatory milestones with traditional FinTech and banking partnerships that reduced uncertainty and opened doors for institutional engagement.

The GENIUS Act, signed into law mid-year, created the first federal framework for payment stablecoins- clarifying reserve requirements, issuer oversight, and consumer protections. After years of regulatory ambiguity that kept major institutions paralyzed on the sidelines, the floodgates finally opened. The response was immediate and massive. Visa partnered with Bridge, the stablecoin infrastructure company that Stripe spent over $1 billion to acquire- launching a card-issuing product that lets cardholders spend stablecoin balances at any Visa-accepting merchant. Visa also expanded its U.S. stablecoin settlement capabilities, allowing select issuers and acquirers to settle obligations in stablecoins rather than through traditional banking rails and business hours.

https://x.com/mastercardnews/status/1946253851012567309?s=46

This is the institutional adoption moment we've been waiting for. It's also when the privacy problem becomes impossible to ignore.

When every transaction is public and traceable, we've accidentally built the world's most surveillance-friendly financial system. For the fintech giants and institutional players who could 10x stablecoin adoption overnight, this is a deal-breaker.

The Privacy Gap in Stablecoin Design

Public ledgers deliver unprecedented verifiability, but they come with a devastating trade-off: the complete elimination of financial confidentiality. Every single transaction exposes sensitive data that would be protected in any traditional financial system. Account balances, payroll information, trading flows, and counterparty relationships all become permanent public record. Anyone with a block explorer can map your entire financial footprint, even if identities are abstracted at the address level.

This radical transparency is killing real-world use cases before they can even get started. No CFO wants competitors reverse-engineering their vendor relationships and spending patterns by analyzing on-chain transactions. When employee salaries become searchable public data, you've created both privacy violations and security risks that no HR department would tolerate. Investment strategies and cash positions get front-run by observers who can see every treasury move in real-time, destroying any competitive advantage institutional players might have.

The irony is stark: we created decentralized finance to escape the limitations of traditional banking, but ended up with a system that exposes users to surveillance that banks would never subject us to.

https://x.com/valkenburgh/status/1980332929034383865?s=46

The Dual-Mode Solution

Most privacy approaches force a choice between public and private tokens, creating UX friction and liquidity fragmentation precisely where adoption demands minimal entry barriers. Wrapped privacy tokens (like shielded pools) require users to bridge assets into separate contracts, losing composability with existing DeFi infrastructure.

The dual-mode concept injects privacy capabilities directly into the token contract, preserving the token’s native behavior while enabling private balances and transactions without wrapping, bridging, or breaking protocol compatibility.

How Dual-Mode Works

In a dual-mode system, the same token contract manages two states:

- Public mode: Standard ERC-20 behaviour, balances and transfers are visible on-chain.

- Shielded mode: Public tokens can be rotated to encrypted tokens, which makes their balances private. Any use of these tokens also keeps the transaction amount private.

The key innovation is that both modes share the same underlying token. There's no wrapped asset, liquidity split or protocol fragmentation. Users simply toggle between shielded or public mode. The dual mode tokens could also be minted as shielded tokens in the first place.

The Advantages

The path forward requires seamless user experience where privacy becomes a toggle rather than a barrier. Users shouldn’t need to swap tokens or abandon their favorite DeFi protocols just to transact privately. The dual-mode concept doesn’t fully solve this today, but it acts as a critical building block toward that goal. The same USDC or DAI should work whether you're buying coffee publicly or transferring funds confidentially. For stablecoin issuers, this means embedding privacy directly into existing infrastructure rather than deploying separate privacy tokens or managing complex wrapper protocols.

This approach unlocks selective disclosure - the ability to meet regulatory requirements through programmable privacy. Transactions remain private from public observers while staying auditable by authorized parties when needed. The risk mitigation benefits are immediate: users can hide large balances to reduce targeting and phishing attacks, while traders can protect themselves from front-running and MEV extraction that cost them billions annually.

Perhaps most importantly for institutional adoption, compliance-ready privacy makes GDPR and MiCA requirements around data protection actually manageable. When financial data isn't permanently etched into public ledgers for anyone to analyze, meeting regulatory standards becomes an engineering problem rather than a legal impossibility. The choice between privacy and compliance disappears entirely.

The Real World Is Not Permissionless

For years, "payments" was crypto's most oversold promise. Every project claimed it would revolutionize how we buy coffee, split dinner bills, or shop online. Most of these promises crashed into the reality that existing payment systems already work pretty well for consumers in developed markets.

But something changed in 2025. Stablecoins stopped chasing consumer retail and instead conquered one of the most broken corners of global finance: cross-border B2B payments and corporate treasury operations.

https://x.com/coinbureau/status/1983959387900375120?s=46

Cross-border transfers emerged as the most mature use case. Businesses used stablecoins to settle invoices, manage international payroll, and rebalance treasury positions across regions in minutes rather than days. For emerging markets, dollar-denominated stablecoins continued to serve as a hedge against currency volatility, but with growing integration into local FinTech platforms rather than informal peer-to-peer usage.

Even with regulation, the idea of institutions using transparent payment rails at scale remains politically sensitive.

Think about what this means for the B2B use cases driving stablecoin adoption. When a manufacturer pays suppliers through stablecoins, competitors can track sourcing relationships, payment timing, and cash flow patterns through blockchain explorers. When multinational corporations rebalance treasury positions, market participants can front-run currency strategies and arbitrage corporate decisions in real-time.

Our Dual-mode toggle could help stablecoins operate in two distinct states: fully transparent when needed for compliance, auditing, or public verification, and shielded when privacy is essential for business operations. Fully Homomorphic Encryption makes this possible by enabling computations on encrypted data.

Here's the real-world usecases it would unlock:

Enterprise Treasury Management

When MicroStrategy moves $500 million into Bitcoin, every competitor, regulator, and market participant can track their exact timing, amounts, and execution strategies in real-time. This creates an information asymmetry - sophisticated observers can front-run corporate moves, manipulate prices around known large transactions, and reverse-engineer entire treasury strategies from public data.

With dual-mode stablecoins, corporate treasuries could execute large transactions privately while revealing only what's required for compliance reporting. Consider Stripe processing billions in merchant settlements - currently, if they moved to blockchain rails, every competitor could analyze their merchant mix, seasonal patterns, and growth metrics by watching settlement flows. Private stablecoins would let them capture blockchain's efficiency benefits without surrendering competitive intelligence.

Payroll & Benefits Distribution

Companies like Bitwage, BitWage, and Request Finance already handle crypto payroll for thousands of employees, but current solutions create an impossible choice: either expose every employee's salary, bonus, and equity distribution on public ledgers, or abandon blockchain efficiency entirely. This isn't just a privacy concern - it's a security risk that creates targeting opportunities for criminals and violates basic employment confidentiality standards. The dual mode would let employers pay salaries in a non-transparent way, while still giving employees an easy way to rotate a desired amount of shielded tokens back to public mode- or example, to buy coffee at a favorite coffee shop that doesn’t accept private tokens yet.

Healthcare & Insurance Payments

Healthcare organizations exploring blockchain payments face strict HIPAA compliance requirements that make transparent ledgers legally impossible for many use cases. When insurance companies process claims, reimburse providers, or settle pharmacy payments, transaction patterns can reveal sensitive patient information even when individual identities are pseudonymous.

Consider a specialty cancer treatment center receiving payments from multiple insurance providers. Current blockchain solutions would expose patient volumes, treatment costs, and provider relationships in ways that violate medical privacy laws. Dual-mode stablecoins could enable efficient blockchain settlements while keeping sensitive healthcare data encrypted, with selective disclosure only to authorized auditors and regulators.

Financial Services Infrastructure

When JPMorgan processes interbank settlements or Goldman Sachs manages client asset transfers, exposing transaction flows would violate decades of established confidentiality standards.

Dual-mode stablecoins offer a bridge: banks could capture blockchain's 24/7 settlement efficiency and reduced counterparty risk while maintaining the privacy standards their institutional clients require. Wealth management firms could execute large block trades without revealing portfolio composition or investment strategies to front-runners and competitors.Private stablecoins would let custodians provide cryptographic proof of reserves without exposing individual client holdings or trading patterns.

Building the Future of Private DeFi

Payment processors have moved beyond "exploring" private stablecoin infrastructure, they're actively building it. The institutional demand is coming from CFOs with explicit requirements for transaction confidentiality. FHE has crossed the performance threshold that separates academic curiosities from production-ready infrastructure. Regulatory frameworks are evolving too.

The GENIUS Act's passage signals that policymakers understand that privacy and compliance aren't mutually exclusive concepts anymore.

We need stablecoin issuers to embed privacy at the token level, not as an afterthought.We need wallets where switching between private and public modes feels as intuitive as moving funds between a checking and savings account. We need compliance rails that meet regulatory requirements without forcing users to give up privacy by default.

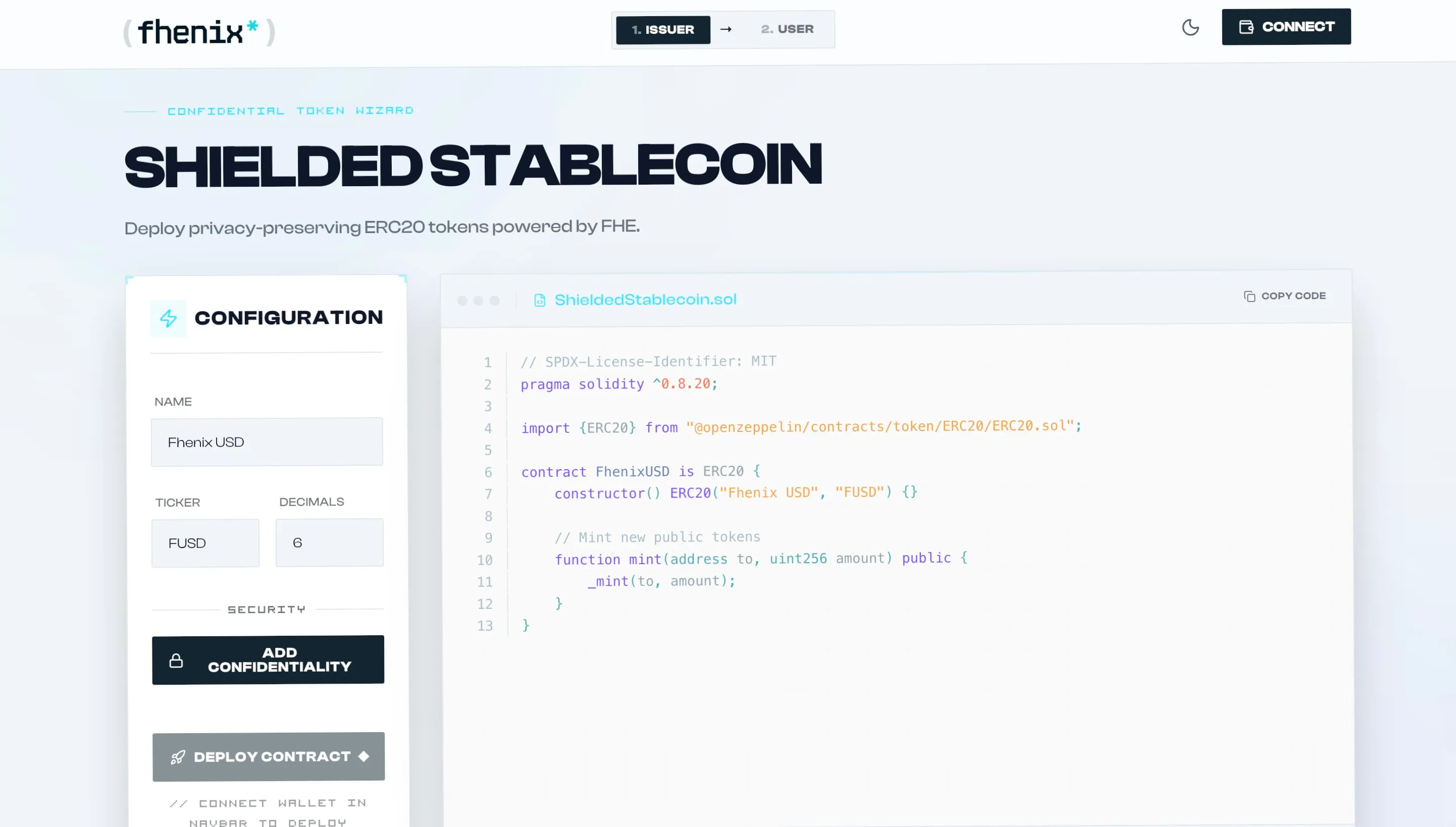

Our shielded stablecoin SDK represents this vision in practice.

Try the demo to see dual-mode privacy in action.

For Stablecoin Issuers: The Shielded Stablecoin SDK demonstrates how straightforward it is to deploy a dual-mode stablecoin. Issuers can enable both public and shielded modes for the same native token without synthetic wrapped tokens. The implementation preserves all existing functionality while adding confidential capabilities.

For End Users: The user interface demonstrates seamless rotation between public and shielded modes. Users can shield tokens to enable confidential balances and transfers, then unshield back to public mode as needed. Minting, transferring, swapping- all work the same. Privacy becomes a toggle rather than a barrier.

In the next episode of Privacy PMF Stories, we explore the CoFHE SDK: the missing layer between powerful privacy tech and real-world usage, and why getting this right could unlock the next wave of adoption.

This is Episode 3 of Privacy PMF Stories where we share what we’re learning about building privacy infrastructure people can actually use.

👉 Want to build with us? Explore our developer docs or join the conversation on Telegram.

.svg)

.svg)

%20(15).svg)